But read past this rhetoric… because he makes some excellent points…

… and if Govenor Newsom thinks he did everyone a favor by raising the minimum wage for fast food employees, he really was just thinking more about politics than actually helping those who need a hand.

To summarize:

Higher employee prices means more automation. i.e., loss of jobs. (He highlighted self-ordering terminals as an outstanding example.)

So the real minimum wage is unemployment.

The wage increase will simply be passed on to the very people who already have trouble making ends meet.

The entire business model for fast food used to be fast & cheap, augmenting ownership efforts with kids and young adults needing part-time and summer jobs.

All Top 10 schools. Now those are some seriously academic schools!

You may ask, “how the hell are some of those schools gonna compete? They ain’t even good at intramurals!”

$50m a year and a global viewing audience showcasing players say they can build a capable sports program in a relatively short period of time.

And if they don’t want to? No worry, we’ve got Dartmouth (#12), Brown (#13), Vandy (#13), and Cal (#20) clamoring in the wings. Which institution wouldn’t want to be part of this? The best of all worlds: Money… TV distribution… and recognition for athletics and academics… on a national stage… coming into your living room weekly.

In fact, maybe we borrow a page out of the Premier League’s playbook: If one of our schools drop out of the academic Top 10 for 4-years running, they can lose their spot to another Top 10 school.

Why?

Because the idea is that this is a power league for TOP academic schools…

… because ultimately that’s what our sponsor would be paying for…

… not only viewing eyeballs for competitive athletics… but access to the hearts & minds of the very kids that are going to shape the future.

UPDATE:

The U.S. New & Report Top College Rankings bounce around… for example, Duke is now ranked #7 and Northwestern #9. But, clearly, the best are annually top rated.

… and if rumors are true, Stanford and Cal will be leaving for the ACC soon.

What a disappointment.

Why is the Pac-12 — and Stanford — operating from a position of weakness and not strength?

Since when did Stanford simply settle?

Why doesn’t Stanford lead the Pac-12 and REBUILD the league… into something new & different & AWESOME?

How about creating a POWER FOOTBALL CONFERENCE that also turns out bright technical students? The kind we want to root for coming out of college. The kind that Google and Apple and Amazon LOVE to recruit.

A power Ivy League.

Before you say, “well, Stanford isn’t exactly a sporting powerhouse,” think again. Not only has Stanford won its share of Rose Bowls (tied for third most wins)…

… but there is this little something called the Directors’ Cup that recognizes the institutions with the most success in collegiate athletics. Since its founding, Stanford has obliterated ALL NCAA Division 1 schools… winning 26 of the 29 cups awarded. (Is obliterated too strong? There are 363 Division 1 schools. So possibly not.)

Back to the task at hand: If you were going to create such an academic/football powerhouse conference, you couldn’t have two better schools than Stanford and Cal as foundational anchors.

And, Notre Dame could use a home, too. Wow… another great football school graduating great students.

We’re almost halfway there… all we have to do is find five more great schools with solid and aspiring football programs out of the 360 NCAA schools left…

… and then the new PAC-8 rides again… let’s call it the Power Academe Conference…

… keeps its old vibe… but with a definitively new purpose: To show the world you can have great sports AND great academics. Strive for the best of the best… or rather, the best AND the best.

So how to finance this new PAC-8?

Easy. Google.

Or Apple.

Or Amazon.

Each has an embarrassing amount of disposable cash…

… and each has their own TV NETWORK…

… the very two things that everyone seems to be chasing.

Did I say an embarrassing amount of disposable cash? Here is perspective: Disney, which owns ABC, which owns ESPN, has about $12 billion in the bank.

Google? $120 billion.

So I’m not exaggerating when I say eight teams x $50 million equals round-off error to these folks.

Why would any of these companies do this?

Hearts & Minds. Of the students. The ultimate societal influencers. It’s that simple. And that valuable.

The “network” crowd — ABC/ESPN, CBS, Fox, NBC, etc. — doesn’t care about that. All they care about is temporary eyeballs.

But tech companies… they care about something much more valuable: FUTURE CUSTOMERS and FUTURE EMPLOYEES.

Sure they’ll get an audience… and content… and these have value…

… but the real value — that has no value to the network crowd — is getting a student to use a search engine FOR LIFE… or an iPhone FOR LIFE… or even create new products that the world will use FOR LIFE.

Because here’s the big secret that these tech companies know: It takes a special kind of person to create world-changing products…

… like the kind Stanford and Cal graduate.

That, as the old TV commercial taught us, is priceless.

That’s why, utlimately, the network crowd can’t compete.

That’s why, ultimately, it’s totally worth a tech titan stepping in with a big swinging diploma.

That’s how Stanford negotiates from a position of strength.Hearts. Minds. The Future. Priceless.

Why, oh why, hasn’t someone called up ex-Stanford President John Hennessey — chairman of the board of Alphabet, Google’s parent — and have him broker this deal? Or maybe Apple’s Tim Cook, who is college football’s #1 fan? Or maybe both… and get them bidding.

Stanford has had a rough few years. But Stanford does not have to settle. Let’s create a conference IN OUR OWN IMAGE.

UPDATE #1:

Some have reasonably suggested that this could take a while to assemble. Fair point.

Then why not just start with the two teams… Stanford and Cal… a dependent independent tandem?

The tech titans might even like that better… because (1) Stanford and Cal are of particular importance to them, and (2) they’ll get to test out this whole “Power Academe” thing.

This would allow the budding PAC-2 time to be incredibly selective. Only the top academic/sports institutions need apply!

And I’ll add one more thing that only we folks in Silicon Valley think about: We’ll OWN the conference. Like a start-up company. Everybody take a moment and wrap your heads around that one. Chaos absolutely brings opportunity.

UPDATE #2:

On Sept 1st, 2023, Stanford and Cal… settled… for the ACC.

Obviously I don’t agree.

But I understand. They felt homeless. And they wanted to keep playing quality teams.

Fine For Now.

And they felt homeless.

Did I repeat myself again? I did. They shouldn’t have felt homeless. They’re Stanford University, one of the top schools in the entire freakin’ world… with the 3rd largest endowment in the world…

… created by their students that created this generation’s technical explosion and previously unimagined wealth.

So how will the ACC work out?

FFN.

At some point, though, Stanford will get tired of being treated like a perpetual pledge, especially if Troy Taylor turns out to be the second coming of Bill Walsh or (dare I say it) Jim Harbaugh.

And, at some point, all this is going to blow up again. Once we started paying amateur athletes to play… and then provided the means to bed-hop annually… well, instability is now the norm.

The left thinks that’s yet another data point that climate change is real.

The right thinks that’s nothing more than the natural ebb & flow of climate through the eons.

Here’s why everyone on the right are idiots about climate change:

Who cares WHY?!

Whether it’s people or nature, everyone agrees on what happens during these ebb & flows: Weather patterns change, storms get more severe, drought increases, polar ice caps melt, seas warm and rise… AND SPECIES — LIKE HUMANS — GET WIPED OUT.

So if we know this, shouldn’t we actually try to do something to slow down the inevitable?

Duh.

Is there a way to do this without destroying our way of life?

Of course.

Here’s something amazing that we learned during Covid: That for that 2-3 month period in early 2020 when no one drove… and people were more careful about their consumption (toilet paper, anyone?)… the planet — literally — was able to breathe again.

This is a fact.

So what if we went back to some of those behaviors that made a material and measurable difference?

Now, I am not advocating shutting down local restaurants and businesses again… far from it.

What I am advocating are some of the simpler changes in behavior.

How about more of a focus on local activities (which local restaurants and businesses will love)… the kind that require no-to-minimal driving… or public transportation… or electric bikes and scooters… or, best, just peddle the damn bike yourself, which is healthy for everyone.

Why not drop the speed limit back to 55mph? We survived just fine in the 1970’s and reduced necessary fuel consumption by about 15%. Literally only adds just minutes to average trip length… less time than you spend dallying in the bathroom a day.

Don’t run a dishwasher or washing machine unless it’s full. Don’t use three paper towels when one will do. Reuse aluminum foil when it’s not dirty just crinkled. Turn lights off when you’re not in a room. Don’t leave the TV running all day & night when you’re not watching it. Don’t keep buying plastic bags at the grocery store. Learn to appreciate left-overs. Open windows and save the air con. Wear a sweater in the house during the winter. Buy an electric blanket and save heating the whole house at night. Etc., etc., etc.

Why not do a bunch of small things… that aren’t such a big deal at all… but help us delay the inevitable?

It’s idiotic that we have to ask people not to jump off a cliff.

Between my parents, only my mom had a brother. So growing up I only had one uncle… my Uncle Nicky.

Sadly, he passed on 29 October 2022.

But he won’t soon be forgotten…

… because my Uncle Nicky was one of those individuals that come around once-in-a-lifetime.

Such a fun uncle growing up! I was forever “The King Fish” until literally his final days. Uncle Nicky invented the “Running Down The Hall” game… where one of my three sisters or I would run down the hall and, to my mom’s dismay, the rest of us would throw pillows and cushions at the runner in an attempt to knock them down and not let them get to the end of the hall. Tackle football had nothing on RDTH! The best kid game e-v-e-r.

As all good uncles do (or should do), he was the first to let me drive a car when I was 12 or 13. But it wasn’t just any car… it was his brand new most beautiful white-with-stunning-red-leather-and-real-wood-interior Jaguar XJ6. Who forgets their first? Not me! To this day one of the most elegant cars I have ever seen.

Besides my dad, Uncle Nicky was probably my biggest entrepreneurial influence. The one thing he did better than anyone (including my dad) was to integrate the things he loved into his life’s work. He never worked… he lived.

Turns out my uncle was a movie guy. Wrote. Directed. Filmed. Edited. Produced. Distributed. And anything in between. He represented everything Hollywood, big and small. I didn’t recognize it at the time, but my uncle was really the very first truly creative artist I knew.

I didn’t know the whole story, but early in his career he was opportunistically successful with more adult-themed movies. He hopped between his homes in California and the French Riviera, but eventually gave that all up so he could be a family man. Most people would find it tough to walk away from that kind of success, but family was all-important to my uncle.

So his life turned… and at times that was difficult on his family… because being an artist and now a provider for a family are tough things to balance. But somehow he made it all work. Sometimes just barely.

In his new professional niche, he often had to get, well, creative. He would use me, my sisters, my mom and her friends, even our classmates and teachers as extras in whatever movie project he was working on. He went through a horror phase and that was a lot of fun for our entire town, getting all ghouled-and-bloodied-up. His cult hit was “Criminally Insane”… about an obese, serial-killing nurse that would get rid of the bodies by — spoiler alert — eating them. Audiences couldn’t get enough! Since he was essentially a one-man show, he’d also use our names, or variants of our names, as cast and crew, just to make his productions feel bigger than they actually were. Ever creative.

I will admit, I tried to be a good actor. But, alas, I don’t think I was doing my uncle any favors. He once cast me as an extra in a western and on a 100 degree day I swallowed a chunk of chewing tobacco. Needless to say production stopped for a bit while I vacated my stomach. But he loved it, especially the, uhm, realism. Said it was a great start to me learning method acting. :)

As mentioned, my Uncle Nicky placed a premium on family. I’ve never seen a more devoted son (sorry, mom!). When my older sister was suffering from the ravages of diabetes, my Uncle was always there for her, driving her around, making sure she attended family gatherings and parties, talking to her on the phone, and in general just making her forget, even for a little bit, her deteriorating condition.

Of course there is always the challenging side of any artist. There were times when we just couldn’t understand his behavior. But mostly I remember my Uncle Nicky being an inspiration. He’d share his latest writing or movie project and it was impossible not to get caught up in his energy. I used to love hearing him pontificate… he’d always weigh in on an interesting topic… and he always had an interesting and especially unique take. At those times I always thought he should be a college professor rather than in entertainment. I guess maybe his magic was he was a bit of both.

My Uncle Nicky taught me life is about what you’re engaged in… what is consuming you… what is fulfilling you… and not to shy away or apologize for it, rather, recognize it for what it is: special. Do what you love… and you’ll never really work a day in your life. I think he single-handedly invented that saying.

My Uncle Nicky was truly the road less traveled.

I know you won’t rest in peace… because I’m sure you’re too excited to get back to work… writing new scripts… enlisting old and new actor friends… getting everyone jazzed about all this Hollywood stuff… all told from, as I’m sure you’re describing it right now, your new heavenly point-of-view.

Somehow I think you’re going to have fun in eternity. :)

We’re honoring heroes today. Which is well and good and proper.

But why aren’t we following in their footsteps… and trying to become heroes, too?

Most of us don’t have to go to war. But we’re still in a war today. Rampant, choking inflation. Climbing interest rates. Pollution. Dependency on the Middle East.

Brave men and women gave their lives for us to have a better world. And when it comes to our big moment to contribute… to be counted on…

… what the hell are we doing?

Squat.

Here’s something you can do to be a hero TODAY: Drive less. Ride a bike. If you have to drive, drive 55.

We ALL can do that. Right now. This very minute. We can reduce our oil consumption by 10-15%.

Let’s throw out the lead foot (i.e., fast starts/stops) and we save another 10-15%.

Why does this make you a hero?

Because we lessen our dependency on oil politics… whether that’s Middle East or in our own backyard.

Because less oil consumption means less pollution.

Because less oil consumption means less demand and therefore falling oil prices. And — CRITICALLY — there is a one-to-one correspondence between oil prices and inflation. Higher oil, higher inflation.

But LOWER oil, LOWER inflation. Everyone has more money in their pockets. Interest rates are lower. Less pollution so everyone is breathing a bit easier, including the Planet Earth.

And just like that… without government intervention… without having to watch the market painfully spiral downward… without really anything more dangerous than a slight change of bad habits… YOU’RE A HERO.

Just like that.

Btw, if you’re someone who’s saying, “forget that, my freedom is the ability to burn as much gas as I please!” … then you’re someone that doesn’t deserve the sacrifice made by our fathers and mothers… because acting irresponsibly does NOT equate to personal freedom… it equates to you being a selfish, unappreciative jerk.

We’re at war… no one is asking you to risk your life… just sacrifice a little bit of speed for a whole lot of good.

(NOTE: This article was published in Seek Alpha on April 19, 2022, sorry for my delay posting it here!)

SUMMARY:

Skillz (SKLZ) announced significant operating changes during their Q4 2021 earnings call, including material cost cutting having to do with ineffective marketing spend.

Cost cutting is critical. But as important is cutting their excessive fee structure (i.e., their “vig”). Because their problem isn’t getting betting players, but rather keeping them betting.

Reducing their dispiriting 50% betting fees to the industry standard 10% won’t affect revenues and could be key to creating sustainable profitability, possibly 1-2 years ahead of guidance.

I have a Strong Buy recommendation on SKLZ.

Thesis

Skillz (SKLZ) announced major operating changes in their Q4 2021 earnings call, including material cost cutting having to do with ineffective marketing spend. This cost cutting is critical. One doesn’t need to look past their Q4 2021 P&L results to figure this out.

But even with cost cutting, bears think this situation is unfixable. That a lot of their revenues were due to “free money” promotions and cutting these will cause revenues to plummet and the company to still crash and burn. Certainly the current share price reflects this.

But, tactically, the situation has a straightforward fix. Simply reduce the vig — that is, the fees Skillz charges bettors — from their current (and dispiriting) 50% to the industry standard 10%. Change the vig, change the world.

Bears will counter getting less vig would cause revenues to drop even faster. But they won’t, because when you run the numbers, nothing happens. Well, check that, something important does happen: The revenues become recurring and sustaining.

For my first look at SKLZ, I wrote an overview piece on the company explaining why it was woefully misunderstood and undervalued and tagged it with a “Strong Buy” (and still have that rating). I did so because the company has just too many things going for it to be trading near gross cash levels, including scalable technology, sophisticated infrastructure, a large, established base of paying and non-paying players, a deal with the all-powerful NFL — and now the wildly-popular UFC — partnerships that are sure to attract other top brands, and 3/4 of a billion in gross cash in the bank. But most important for a growth company in this market: An achievable path to profitability.

But it doesn’t have profits right now, which is what the market wants to see. This article examines Skillz’s cost cutting in more detail and its potential effect on profitability, including ways to accelerate profitability 1-2 years ahead of guidance.

Understanding The Other Two Important Numbers In SKLZ’S P&L

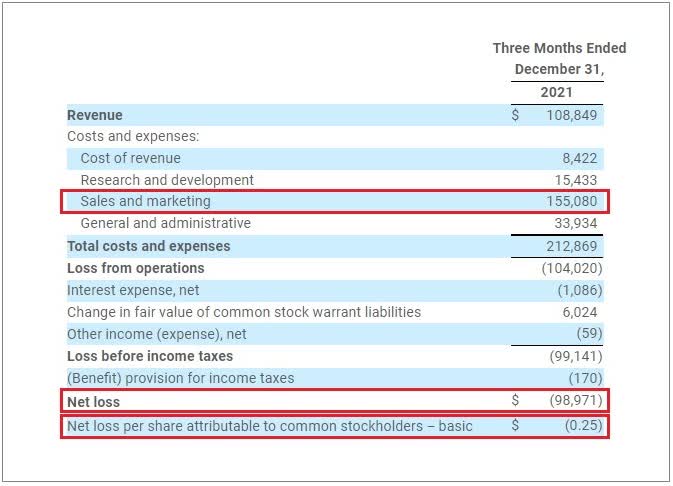

Certainly revenues and profits are important numbers in any P&L. But what drives those numbers? And in particular, what drove the gaudy $155 million Skillz spent on Sales & Marketing in Q4 2021?

The company is now committed to cutting User Acquisition and Engagement Marketing costs. Which is great and needed news. But the relevant question is why did Skillz feel the need to spend all that money in the first place?

Of course there was great pressure to continue growing its player base. Like many companies, Skillz was simply offering customer incentives in an effort to kick-start players… the same way it did all through 2021… only accelerated in Q4 in an effort to end the year with a bang.

However, what it really was doing — what it has been doing for a long time now — was trying to make a premium but non-standard fee structure work. While throwing gobs of money at players did accelerate the top line for many quarters, the “easy money” environment was also distracting from what was happening to the bottom line: Trouncing it.

Every company needs to incent customers, but after spending nearly half a billion on just marketing in 2021 — compared to less than $400 million for all of 2021 revenue — Skillz now has more than enough proof that its old approach doesn’t work. Let’s talk about why.

Engagement Marketing That Didn’t Stand A Chance

I’ve always loved the old joke, “The beatings will continue until morale improves!” It kind of reminds me of Skillz pushing “promotional cash” at players and, like the joke, no matter how much promotional cash Skillz doled out, it just wasn’t improving the bottom line.

That’s because it’s not the amount of promotional cash that’s the main issue — that actually did a fine job getting players to open their wallets (as unnecessarily excessive as it was). It’s Skillz’s vig — their commission — that’s chasing away paying players once they start betting. It’s way too high. Impossibly high. It’s literally that simple. Change the vig, change the world.

Let’s review: The betting action in a Skillz game — for example, their new NFL 2-Minute Football — is intoxicating… addictive… exactly what you love to see in a legal vice investment. SKLZ is ringing the cash register twice every 60 seconds. Each player wagers a standard $0.60 “entry” fee and Skillz rakes $0.20 every game play. Betting players play on average almost a couple dozen games a day, so the games — and fees — add up fast.

Wow, sounds great if you can get it! But that’s the problem, Skillz isn’t getting it for very long. This is what a Skillz wager looks like to anyone that understands betting — like every NFL and UFC bettor in the world:

Standard bookmaker “vig” vs. Skillz. (The Lone Contrarian’s calculations.)

That graphic says it all, eh? It answers a lot of questions important to the success and/or viability of the business, for example:

Q: Why aren’t players buying in more (i.e., recurring revenue challenges)?

A: Because it’s impossible to win when the house is taking 5x the standard % rake.

Q: Why was Skillz’s Engagement Marketing “free cash” promotions ineffective in incenting players to buy in again?

A: Because whether I play with my money or their free cash, I’m going to stop betting once the money’s gone. Impossible to win. One and done.

Q: Why does Skillz have so many non-paying active players?

A: Because players love their games, but not their fee structure… so when they’re done getting hit over the head with a 5x vig, they just continue playing for free. If you are a Skillz player, you know this to be true.

But this is easily fixable: Just change the vig. That simple. Change the vig, change the world.

Bears are probably screaming now, if you change the vig from 50% to the standard 10%, revenues will crater!

This is why I believe bears don’t really understand this company. That isn’t the way betting works. That isn’t the way mobile gaming works. That isn’t even the way the numbers work. Run the numbers, nothing changes. The revenues stay the same. Well, check that, something important does change, the revenues become recurring. The golden ticket to a sustainable business.

Let’s quickly look at the math: With a 50% vig (what Skillz has today), a $10 buy-in, and evenly-matched games, a bettor playing the $0.60 “Regular Season” game will win $0.40 half of the time and lose $0.60 half of the time. That’s an average loss of $0.10 every game. So $10 buys you 100 plays, not even a day’s action for some players. And at the end of those 100 games, the house’s take is $10. Because the vig is so high — and it becomes apparent that it’s impossible to win — players don’t buy in again. But they do keep playing for free.

If we change the vig to 10%, guess what, the house’s take is still $10. The only difference is it takes more games for the house to earn the same amount of money… but — and this is the critical piece to understand — these are games that are going to played anyhow whether they’re betting games or on the free practice field… as evidence by Skillz’s sky-high84%active-but-non-paying player percentage. Changing the vig won’t even affect the performance of their network… because Skillz is already serving these games.

50% Vig vs. 10% Vig: The house earns the same either way. (The Lone Contrarian’s calculations.)

I’m sure Skillz was hoping it could charge a premium. After all, what they’re doing is so new. And exciting. But it’s just not working. Bettors know better.

Skillz seems to have forgotten the basis of what I consider its break-through business concept: Instead of just making mobile games and struggling — like the zillions of other aspiring game developers — to charge for game play, they tried to solve that problem for the entire industry by creating a development platform that positioned game play as something brand new in gaming: A legal wager. Brilliant!

But critical to that concept: A bettor wants to win money. That’s why they’re betting. But it’s virtually impossible to win against Skillz’s 5x rake in an evenly-matched game. Almost all of the players always lose. And quickly. So it can’t be anything else but one and done. Because betting may not be the smartest thing to do, but even the craziest of bettors figure out when the deck is stacked so completely against them.

So Skillz built a fantastic company with fantastic technology and a fantastic infrastructure, all based on a brilliant idea, and they did all of that and then spent a huge amount of effort and time and cash just getting a player to the money table… only to… what? Chase them away to the free games because of an impossible 5x rake?

It’s time to share the key insight here: Skillz players want to bet. They just invested a lot of time becoming hot stuff at a Skillz game. All SKLZ has to do is not stack the deck against them. Give them a standard vig — one that every bettor is used to — and one that’s been in use since betting was invented, a vig that every bettor thinks they can overcome. If I don’t feel like the deck is stacked against me, I like to compete (that’s why I’m playing video games in the first place) so I’ll buy-in again… because playing for money is just more fun than playing for fun. Buying in again… and again… and again… is the very definition of healthy recurring revenues (as ironic as that may sound :).

The good news is Skillz can easily change their vig — without affecting revenues — literally overnight. And the $56.7 million they spent on Q4 Engagement Marketing? Most of that gets saved overnight, too.

From a revenue point-of-view, there’s another enthusiastically welcomed upside: SKLZ has 3 million active, non-paying players… and many might love to bet again if said deck wasn’t stacked against them. Bringing a big chunk of those 3 million active, non-paying players back into the betting fold would put a JOLT into revenues, eh?

But also MONUMENTALLY important: Skillz must lower the vig before the mass of NFL bettors enter the picture. The sooner the better. Because NFL bettors are savvy and won’t stand for paying a 5x rake. The NFL opportunity will otherwise be D.O.A. and Skillz will have snatched defeat from the jaws of victory.

(* A nod to Mel Brook for a variation of a famous quote from his 70’s classic, Blazing Saddles. : )

Why did SKLZ spend almost $86 million on new customers when it has about 3 million unmonetized players — players who love their games enough to still play actively? They might have also forgotten that the easiest customer to get is an existing customer.

Let’s put this in perspective: If they figure out how to get 1-in-5 to pay the average, they could double revenues. Organically.Sustainably. As suggested above, changing the vig can do this all by itself (and more). Change the vig, change the world. But there’s more revenue to be found here.

Because while this may sound odd to bettors, there are some people that don’t want to bet… they only want to play free games. So figure out how to make money from their free play. It’s not like that’s new or anything, much of the mobile gaming industry already relies on monetizing free play. For example:

* How about that time-tested approach, having players watch a rewarded video before a free play? (Maybe give them a 30-day grace period, get ’em hooked, then start showing ads.)

* And that other time-tested approach, paying a cheap monthly subscription so you don’t have to watch ads. This is the subscription generation after all.

* In your multiplayer games, how about selling game skins, Leaderboard animations, dances, badges, and such? That seems to work nicely for free games like Fortnite.

* Even something as trivial as a tip jar can turn out to be a revenue contributor.

But maybe as important: How about creating new kinds of money games… designed to attract non-bettors?

Maybe enter a $1 non-bracketed tournament that happens every hour… where I can play 120 other evenly-matched competitors. We all play three games and the top 10 averages divvy up $100… spreading it out a little bit just creates more excitement, happiness, and engagement. Maybe the next 10 participants get Ticketz (Skillz’s virtual currency)… and — as all gamers know — there are bragging rights for making a Top 20 Leaderboard. As a player myself, I love those odds for a buck. I just took a break from writing this article, played three games, and kicked butt.

How about a “Daily Subscription Tournament”? Pay $9.99 and your subscription gets you into a month of daily non-bracketed tournaments — that’s just $0.33 a day. Same as above, everyone plays three games, but the top 10 averages divvy up $1,000 and the next 90 participants get Ticketz. More bragging rights, happiness, and engagement.

Feel free to shorten the $1 Tourney cycle time, or run a different Subscription Tournament for each hour of the day as participation dictates. By holding these daily tournaments, you just know I’m going to be on the free practice field a lot, so that supports the other monetization techniques discussed above, too.

With over 3 million active, non-paying players, Skillz doesn’t have to look beyond its own registration list to get new paying players. And shouldn’t. If for no other reason, they could have their hands full with new players come this fall when their NFL partnership kicks in. Right now, though, keep cutting most of your $85.6 million User Acquisition spend, it’s not needed. This literally could turn the entire quarter around by itself.

So What Does This All Mean For The Numbers?

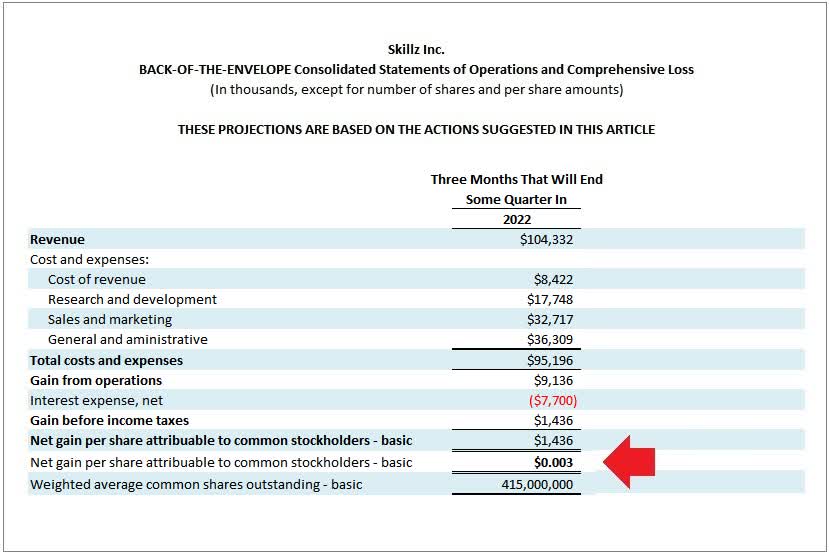

Glad you asked. Here’s what 2022 Q4… Q3… or even Q2 could look like:

Back-Of-The-Envelope P&L Projections for SKLZ in some quarter of 2022 based on the actions suggested in this article. (The Lone Contrarian’s projected calculations.)

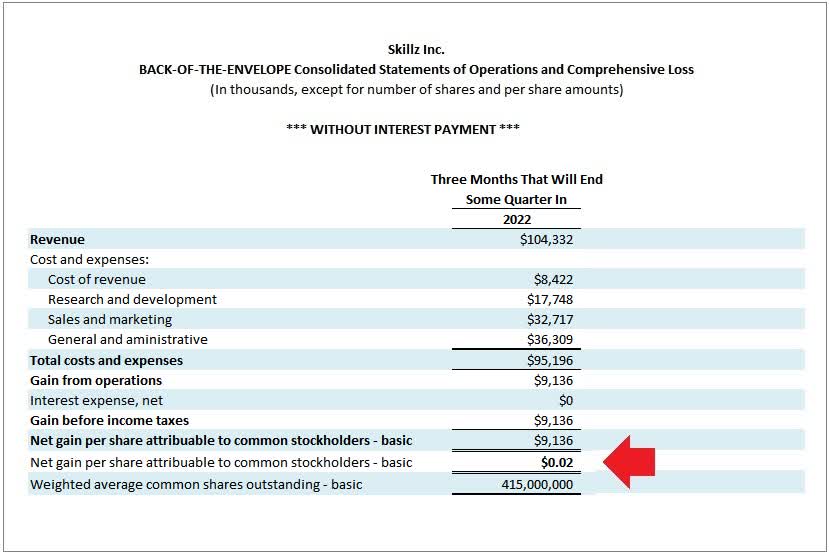

Same Back-Of-The-Envelope P&L Projections as above but without interest expense. (The Lone Contrarian’s projected calculations.)

Assumptions:

* Baseline revenues are Q4 2021’s RAEM (Revenue After Engagement Marketing) and to be conservative I assume no increase (vs. Skillz guidance of “above 30%” growth). Recall that this metric is essentially “net revenues,” i.e., doesn’t include any promotional money in the tally.

Reducing the vig means getting to invite past betting players to wager again. I’m assuming 1-in-5 will try their betting hand again… remember, these are players that want to bet again. So that doubles revenues to $104 million.

I am not, however, including any other recurring buy-ins, digital advertising revenues, newly created cash games, or any revenues from the NFL partnership. Note: I am not including these because the goal was to see the effect of cost-cutting activity on profitability. Clearly, though, I feel strongly that all of these efforts can drive additional, significant revenues.

* I’m using costs from the December 2021 quarter as a baseline.

* Revenues are decreasing from Q4 2021 but we’ll still keep Cost of Revenues at Q4 2021 level.

* Baseline costs include a 10-15% increase in employee compensation, New User Acquisition cut by 80% (and, per company comments, Aarki to save 30% on the remaining 20% that is being spent), and Engagement Marketing cut by 80% (and Aarki again to save 30% on that remaining 20%, too).

* I added $7.7 million per quarter for their Dec 2021 $300 million financing that carries a 10.25% interest rate.

* For this back-of-the-envelope exercise, I’m not including any “Change in fair value of common stock warrant liabilities”, “Other income (expense), net”, or “(Benefit) provision for income taxes”.

What’s It All Mean?

Profits!

OK, to be clear, it’s back-of-the-envelope and just $0.003 per share for whatever quarter they decide to change their vig, which isn’t even rounding error to a penny. But given that the average Wall Street analyst is predicting a loss of about -$0.15 per share per quarter… any profit should quiet those that believe the company is going to run out of cash soon.

As important: Without their big interest payment, they have a profit per share of $0.02.

Fun to think what adding more recurring revenue (especially from the 3 million active but currently non-paying players), digital ad revenue, revenue from newly created cash games, and NFL revenue (!) can do to SKLZ’s top line. Jumps by leaps and bounds, as does its bottom line. But that is for a future article.

But it all starts with reducing the vig. Change the vig, change SKLZ’s world. In this case, the results could be moving up profitability guidance 1-2 years.

I like the Skillz exec team and for all I know they’re way ahead of me with all of this. Or have figured out an even better cost-cutting and monetization approach. But what I wanted to illustrate in this article is with just a few easy levers pulled, we can already see a dramatic difference to SKLZ’s bottom line in a short period of time. It’s why I continue to think this company is woefully misunderstood and undervalued.

Will Smith’s son, Jaden, tweeted this after his dad’s despicable behavior at the Oscars:

And That’s How We Do It.

There were about a dozen different ways Will Smith could have protected his wife’s honor in an honorable way.

But this is what he’s dishonorably taught his son: Violence Matters.

I’ve always loved Will Smith movies. He’s always been such a positive role model. He now needs to voluntarily give up his Oscar so that he can teach his son — and all the other sons out there — that violence is never the answer.

Doing so would convince me that he is truly sorry for the way he handled this situation — and I think second chances are important in life… most especially now with this dangerous and damning “cancel culture” that has infested modern society.

However, if he chooses not to, I’m not sure I’ll ever watch another Will Smith movie again.

To paraphrase Hollywood and Spider-man: “With great fame comes great responsibility.”

P.S. Btw, I was never a big Chris Rock fan… but he just zoomed to the top of my list.

(NOTE: I wrote this article last week when SKLZ hit $2.16. It was just published in Seek Alpha today. Of course it belongs in my blog, too. :)

SUMMARY

People like to bet. Skillz lets people legally bet on their video game play and win money. It’s an entirely new form of entertainment and growing like crazy.

In this volatile market, the SKLZ stock has suffered about a 95% drop in value and is now trading at “going-out-of-business” levels.

But Skillz is not going out of business. They have created valuable assets and their cash burn can be cut quickly (which has already started).

Skillz’s upcoming NFL deal merges two strong money-making themes — betting and playing video football games — and is a strong driver of future earnings.

A Strong Buy.

Thesis

Skillz (NYSE:SKLZ) is woefully misunderstood and undervalued. There, I said it, someone had to.

Misunderstood because investors think it’s a video game company, when it’s actually much more than that. It’s also an enterprise software company… and a legal bookmaker for video games.

Undervalued because investors think the company will run out of money and are pricing it at near-cash levels. But an analysis of their cash burn, combined with operating statements made by the company during their recent earnings announcement and Investor Day calls, suggests otherwise.

Fall From Grace

Skillz has had a painful decline, culminating in a dramatic fall the day after announcing Q4 2021 earnings, crashing just under 20%, but at one point heading to a 40% shellacking.

Sure, it’s not just SKLZ that has felt the pain. The whole market is down, with Nasdaq entering bear territory in early March. Gone are the days of easy money, where the market was handsomely rewarding “growth at any cost.” As long as you were continuing to grow, your stock kept appreciating and if you ran out of money, you just floated a secondary offering at your elevated stock prices and, voila, the market gave you more money.

Maybe it was the end of the trillion dollar giveaways reducing liquidity in the market; or maybe it was rising deficits and oil and inflation and interest rates; or maybe it was bombs dropping on Ukraine and Russia receiving sanctions that inevitably will send ripples through the world’s economy, but the market changed in Q1, and “growth at any cost” was now replaced with, “you better have everything you need to survive because you ain’t gettin’ anything more from us.”

The market doesn’t think so right now, but Skillz is one of the companies that has everything it needs to survive… and thrive.

Why This Company Is Special

Most investors think of Skillz as a video game company, and they do have several in-house games, but they are much more than this. Their primary focus is to provide an enterprise gaming platform for other software game developers. Making a game isn’t easy. But the technical requirements to create a scalable enterprise gaming platform – one that handles billions of games per year – goes way beyond simple game construction. Big barriers-to-entry here.

Further, the enterprise gaming platform that they’ve built has an innovative business model. Advertising networks created a massive digital ad industry arbitraging between a buyer and seller of digital ads. Likewise, Skillz acts as an intermediary between two similarly-skilled players in a video game competition and takes a percentage of their “entry” fees.

Said another way, Skillz allows two players to bet each other… with Skills acting as the “house”… a.k.a., the “bookie.” And as it turns out, there is more upside to being a bookmaker in this particular market than may meet the eye. Imagine an enterprise software company that figured out how to become THE bookmaker for the ENTIRE video game world. That’s Skillz.

Online Competition Content Much Larger Than Offline

While traditional sportsbooks allow you to bet on football, basketball, soccer, and maybe a handful of other physical-world sports, Skillz is the bookmaker for potentially every video game in the world. The content for their potential market dwarfs what a traditional sportsbook can ever hope to address.

For example, you might be familiar with a new game causing quite a sensation called Wordle. It didn’t exist several months ago. But now it has millions of players. It’s a game that was created out of digital bits & bytes, i.e., thin airthin air. And it’s only a matter of time when, with Skillz, you’ll be able to bet someone you can solve the secret word in fewer guesses than them.

This shouldn’t be a surprise, though, hit video games are created all the time. But when was the last time a new physical sport was created that you could wager on? Not for a while. Skillz is the only betting game in town that has the potential to take advantage of an ever-expanding universe of digital content.

What Everyone Missed From The Conference Call

One of the two most important statements in Skillz’s most recent conference call wasn’t when the company said they had a lot of money in the bank (gross almost three-fourths of a billion dollars); or solid revenues, almost $109 million for the quarter, up 61% from last year; or 610,000 paying players, up 56% from last year.

It was when the company said, “… and we’ve been listening to your feedback.“ Andrew Paradise, CEO, attributed this to shareholders. Maybe. But we also all know it was pretty hard not to hear the market crushing the life out of the stock price, too. Regardless, he continued with a welcomed statement for any public company operating today: “… we will transitionfrom our strategy of revenue growth at all costs to increasing profitable growth and efficiency.“

And the second most important statement… the one that everyone seems to have missed? Casey Chafkin, CRO, saying in context to reducing marketing spend, “… the result of that is going to be, and already is…”. That is, that the transition away from “growth at all costs” has already begun.

But can they really turn on a dime? Those that run businesses know they can. Because unlike headcount, facilities, or equipment costs – areas that are hard to cut and where it takes time to see savings – 73% of their 2021 costs were attributed to “Sales and marketing”… and many of these costs are straightforward to turn off.

You literally say, “stop,” and they simply stop. Chafkin even confirmed that on their March 15th Investor Day webcast.

Further, Skillz shared their exactnew user acquisition costs for Q4 2021, $85.6 million. Compare that to their reported $99.0 million loss for the quarter. Knowing the bulk of this spending was ineffective and is now being cut, imagine what Q4 earnings could have looked like if they started cutting last quarter. Revenue would not have been impacted much, but instead of a ($0.25) per share loss – with a ($0.10) expectation miss – it might have been a $0.10 beat… and optically more important, a ($0.05) loss would have seemed tantalizingly near breakeven. That’s hardly a company going out of business.

Actually, that would be a company way ahead of plan.

Net Loss would have looked quite different if ineffective new user acquisition costs weren’t a part of the Sales and Marketing expense line. (Source: Skillz Q4 2021 Earnings Press Release)

Since Chafkin also confirmed in the Investor Day Q&A that the actual cutting started in early Feb, we now could see up to a $40 million savings, or up to a $0.10 per share beat in Q1 2022 results, too. That would be a nice surprise for a stock that could use a nice surprise.

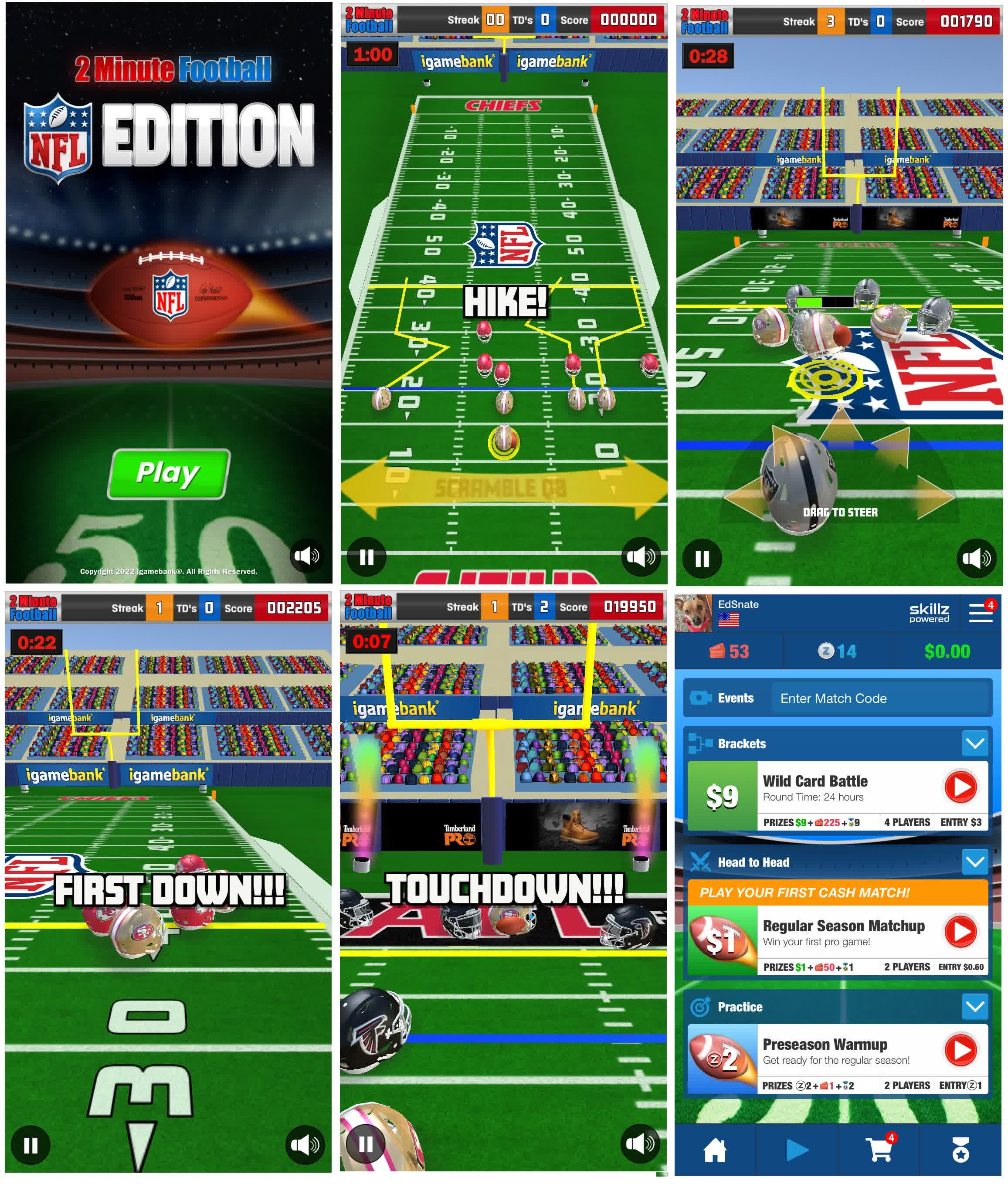

Driving Future Earnings: The NFL

A winning combination: Betting and playing mobile football games. (Source: Actual screenshots from one of the new NFL games that is betting-enabled via Skillz.)

It’s no secret that people like to bet on football. And it’s also no secret that people like to play football video games like Madden. Capitalizing on these, SKLZ has forged a partnership with none other than the NFL and are working with game developers to create NFL-branded football games that let you bet your opponent. Seriously, can you think of a more perfect union than playing NFL video games and betting?

I know many have reported on this strategic partnership but not in this way: That this is an incredibly compelling betting proposition. Betting will go together with video football games like, well, real football and betting.

Thinking about SKLZ as a bookmaker invites new valuation comparisons. One of the monster sportsbooks is DraftKings (DKNG). Both DraftKings and Skillz are online bookmakers. But one takes book for physical-world games, the other for digital games. And while DKNG has about 3x the revenues – and only about 2x the cash – DKNG is valued about 7x greater than SKLZ.

This suggests that either DKNG is trading over twice what it should be or SKLZ is trading at less than half. Given DKNG has more than 3x the analyst coverage, it’s more likely they’re better understood and it is SKLZ’s valuation that’s amiss by half. But I don’t think this is a fair comparison because Skillz has material advantages over DraftKings. DKNG has limited physical-world gaming content they can monetize, while SKLZ’s has virtually unlimited content potential.

Both may be considered bookmakers, but DKNG’s action is considering gambling and thus they have vastly more regulatory requirements and legal expenses. However, SKLZ’s action is not considered gambling, so Skillz doesn’t bear those costs, a significant advantage.

And DraftKings has tons of competition. They have to spend heavily to get into a market and heavily to protect it. Skillz has zero competitors, they invented their market. An awesome – and rare – advantage in business. So comparing SKLZ to DKNG might provide an initial valuation adjustment, but the more you dig into the business details, the better SKLZ looks. Translation: SKLZ shouldn’t be trading at less than half the sales multiple of DKNG, it should be trading higher than DKNG’s sales multiple.

And, per the conference call, they’re working on improving existing player environment and social features. That’s company speak for getting more money out of each player. Typically they could see a 50% lift from these kinds of activities – in fact, SKLZ actually bought one of the domain experts in this space: Aarki, so it’s pretty conservative to project a small 10-15% bump to ARPPU (Average Revenue Per Playing User). That would jump revenues to about $480 million to $500 million.

And, as the company pointed out multiple times during their Investor Day, their guidance does not include the upcoming new NFL games. We can use existing data to help us project future potential here. Just three games accounted for almost 80% of SKLZ revenues in early 2021, or nearly an average of 27% each. It’s important to note that these games do not have household brand names… like the NFL has. So it’s not unreasonable for SKLZ’s NFL games to achieve at least a similar average acceptance within the Skillz player base. As such, and factoring in about half-a-year of contribution, betting on NFL video games could add another 10%-15% to the top line, which pushes potential 2022 revenues to a $525-$565 million range. Right back to the initial forecast, eh?

Yes, there will be some existing player churn. But not included in the analysis above are any additional players SKLZ brings on due to the NFL helping to promote. The NFL has a really BIG megaphone, so of course Skillz will see new players… in fact, the numbers could actually rip much higher. What I think the analysis above says, though, is even looking at it pretty conservatively, their 2022 revenues could still be closer to $550 million than $400 million. Which of course no one is now anticipating.

Revising Misunderstood Price Targets

A few analysts lowered the price targets for SKLZ after their earnings call. The low is now $2.50. My range is $9.00-$12.00. This may be disappointing to those that purchased at higher levels but please know I think this is just over the next six months, so SKLZ will go higher as the company continues to prove it can execute along its new path. And, at least in the short term, it’s a nice opportunity for everyone else. I get to my range by adjusting SKLZ sales multiple to that of DKNG, increasing by 50% to reflect my higher 2022 revenue estimate, and noting that SKLZ’s short % of near 20% is scary high… which inevitably means overshooting when everyone rushes in to cover.

Risks

I think Skillz has been misguided in their big picture customer acquisition strategy. I believe it would be more effective if they spent less time trying to acquire individual players and more time trying to acquire gaming partners and require them to market to their individual players. After all, money is flowing to their partners.

I know many investors may want me to claim that Skillz’s recent $300 million debt financing was misguided as well. After all, it was taken at an eyebrow-raising 10.25% rate. But given that the secondary market has now slammed shut, it feels more like management had a bit of foresight to sock away some extra $’s. With interest rates on the rise, who knows, we might look back and think the money is not all that expensive after all. Don’t forget, with the way they’re now operating the company, they may just surprise everyone and pay it back early.

Churn always worries me. It’s usually bigger for non-betting app games, but smaller for betting games like casino slots and such. If it’s close to the betting norm (1-2%), then I’m less worried.

The real lingering uncertainties I have revolve around the NFL. Are the new NFL games fun and competitive? And what is the business relationship with the NFL? Do the economics allow SKLZ to make a healthy profit; or did they have to sell their soul?

I’m actually OK with the first uncertainty because there are a lot of popular football games to serve as models… and I believe the added, all-important betting component will prove irresistible. People just like to bet on football and play football video games. I am worried about the second uncertainty, though. Having negotiated a partnership agreement with a professional sports franchise in the past, I know they can be quite one-sided. Since the NFL games are the key to the future, bad NFL economics could slow that future down.

Many investors are wondering if SKLZ can turn things around. Here’s something interesting to consider: Skillz actually has the word “frugality” in its corporate values statement. This should give all investors an idea of what kind of guy Paradise is… because that’s not a very glamorous word (i.e., who wants to work for a frugal company?). So if he put it in such a visible place as the “About Us,” it’s genuine. I’ll go even farther and say running a tight ship is in the CEO’s wheelhouse… because he’s a repeat, successful entrepreneur, so none of this is new to him.

So I don’t think the company is going to run out of money like most analysts think, which, ultimately, has created the opportunity here. From trading at about 50x sales about a year ago, SKLZ is now trading at near gross cash levels. What that says is the market is valuing all the rest of the stuff in this enterprise software company – a proven model, scalable, sophisticated technology and infrastructure, an established base of paying players, great multi-year growth, an achievable path to profitability, and a deal with the all-powerful NFL that is also sure to attract other top brands – at just about nothing.

Honestly, at these levels, and with these assets, I don’t know why some enterprise, gaming, or sportsbook outfit is just not trying to acquire them… in the same way I scratched my head that no one picked up Apple when its stock was depressed in 1996. And we all know how AAPL eventually did.

The CEO uses more acceptable language when describing the mission he’s on: To become the “competition layer” of the Internet. That’s fancy but I think investors might like my description even better: To become the bookmaker for every video game on the planet.

That sounds less like a bet and more like a winning investment.

I think every American was heartened at the speed that the U.S., and the free world, levied sanctions on the totalitarian regime of Russia.

A few weeks ago, many said we couldn’t turn off Russia’s access to Swift, that would be the equivalent of an economic nuclear strike.

Then BAM! The EU said, “we’re doing this NOW, please join us.”

Many said we couldn’t stop buying Russian oil, because that would hurt the world, including the EU, way too much.

Then BAM! We stopped buying Russian oil.

Just a few weeks ago, who would have thought so many company would join the battle? Google. Facebook. Twitter. Visa. MasterCard. American Express. PayPal. Nike. Adidas. McDonald’s. Starbucks. Coke. Pepsi. Hundreds and hundreds more… all flipping the middle finger to Putin. In fact, if you haven’t stop doing business with Russia yet, something is wrong with you.

China’s reaction to all of this? Silence in the beginning. A lot of folks say that’s just their way, “to observe.”

I think it’s something different. That they originally thought what Putin thought: “No way the U.S. and the EU can ever get their stuff together to act in concert… and certainly whatever they do won’t have teeth.”

But both Putin and China were oh so wrong. The outpouring of support for Ukraine? STUNNING. BLINDING.

UNANIMOUS.

So China went from quiet cockiness to silent terror… now knowing that the free world has a NEW weapon against oppressors: We’ll just turn you off.

It couldn’t have happened 20 years ago… maybe not even 10… but now the world is really so interconnected, that it really is possible to, say, strangle Russia-the-dictatorship-that-oppresses-people to economic death.

With all this momentum, China realized it had to do something.

Of course they didn’t do what would have been truly helpful to peace… and that is whisper in Putin’s ear, “wtf, it didn’t work, stop acting like a madman!”

Instead it’s s-l-o-w-l-y been rolling out support for Russia over the last week or so. Essentially “reminding” everyone we need to de-escalate because it will further mess up global supply chains and such.

Boy, did Xi miscalculate on that one, too.

Talk turned today of “secondary sanctions” against China. If they’re still doing business with a murderous dictator that wants to take away others’ freedom, then maybe we’ll just turn China off, too.

My reaction?

YES! LET’S DO THAT! NOW!!

Then I got to thinking, why wouldn’t we do this? China is mostly a one-way relationship: They economically abuse us. And every time we ask them to play fair, they cry about it.

Then I got to thinking some more: Which American companies would get hurt by this?

And then it hit me: Apple. The world’s most valuable company. The company that derives 19% of its revenue from China. The company that makes almost HALF of their iPhones in China.

This would be an economic disaster of epic proportions for Apple stock.

And since virtually EVERY person on the planet either has money directly in Apple… or their mutual fund does… or their 401K does… or their bank does where they save their money… and so on…

… hurting Apple stock is akin to hurting every person on the planet.

I kid you not.

Remember the dotcom crash? It started (imho) because Microsoft and Intel, the two companies that used to financially represent everyone in the world, missed earnings numbers and sent shock waves through the financial markets. A history-making crash.

So it’s happened before.

We survived… but remember it was awfully rough for a while… and Microsoft stock price, literally, flat-lined for about the next decade.

If sanctions move to China — whether it’s for their support of Russia — or they start moving on Taiwan — I know every American will feel the way I do: YES! LET’S DO THAT! F*ck China. You sell to your oppressed people… and we’ll sell to the FREE world.

If that happens, I’m not sure Apple wouldn’t get caught in an awfully bloody crossfire.

Certainly all the uncertainty in the world isn’t helping.

But gas prices have skyrocketed. Which means inflation is skyrocketing, since the price of a unit of energy affects everything we purchase.

It’s killing me that all the DRILL DRILL DRILL folks are coming out of the woodwork and screaming, “we told you so!”

It’s killing me because, lest we forget, climate change is absolutely an existential threat to our very existence, too.

Seriously. Next time we get back-to-back “once in a century” storms, you’ll remember how much climate change sucks.

Or, just look at pictures of Beijing at noon to remember just how disgusting pollution is.

Now, we’re contemplating banning the import of Russian oil. And for some reason, this has spooked the oil market even higher.

Really? They supply about 5% of the world’s oil. Only about 1/2 million barrels a day to us. Why the hell do we need to drill more? We’re already exporting 17 TIMES that amount every day!

Maybe we should ask our national oil producers to keep U.S. oil in the U.S.? Or maybe they should just know to do that, as in, knowing the right thing to do in this situation?

AND… maybe the entire world doesn’t have to freak out about a lousy 5% of oil… how about we all just use 5% less energy? Walk to the store? Ride a bike to school? Use public transportation? Carpool? Take one car to a restaurant rather than two?

Seriously, simply combining weekly errands into just one or two trips a week would probably do it.

C’mon, America. We can tell Putin where to shove it AND help clean up the environment with so little effort… it will hardly feel like the WARTIME we’re in.

I’m not suggesting we go into lock down, but there certainly were a few unintended yet welcomed consequences from the early days of Covid.

We learned that we could work remotely, at least those in corporate America.

We learned that we could hold meetings — work or personal — quite reasonably on Zoom.

We learned that even a month of reduced driving made a big impact on our environment. CO2 levels started coming down. You could see fish in the Venetian waters again. And all kinds of other miraculous things, too.

Most importantly, we learned that even a month of reduced driving made a big impact on oil supplies and gas prices…

… and since the price of a unit of energy affects the price of everything else in our world, we were reminded that the price of everything in the world comes down as oil prices come down.

So if I were the President of the United States, here’s what I’d do:

(1) I’d gather the top 50 employers in the country to an emergency meeting at the White House… hey, I can do that, I’m POTUS! :) I’d remind everyone that we’re in a time of extraordinary crisis… whether it’s Ukraine, Russia, China, inflation, deficits, interest rates, supply shortages, pandemics, whatever. I’d ask the CEO’s of all of these companies if they would consider voluntarily having their workforces work at home, just like they did during the early days of Covid. I’d suggest 90 days, to correspond during the spring, where temperatures would not be too cold nor too hot, so easy on home heating and/or cooling needs.

(2) I’d address the nation… and remind all Americans that we’re in facing multiple, life-changing crises… and just like great Americans have done through difficult times, we all can make a contribution. Nothing is locked down. But walk to a local restaurant or shop. Ride your bike to school. Take public transportation. If you have multiple cars and have to drive, take the one that gets the best gas mileage. Plan trips better, do all your errands in one trip rather than three. Get together with your friends and neighbors and carpool when possible. Want to show solidarity with the Ukrainians? Want to stop run-away inflation and pay less money for everything? Want to put a lid on pollution? Want to sock it to Russia (and the Middle East while we’re at it) where it hurts, in their oil pocketbook? For the next 90 days, let’s make a wartime-effort to reduce or eliminate driving if we can.

(3) I’d met with the leaders of other countries, talk about what we’re doing in the United States, and ask each and every country if they would join the battle.

Here’s what I love about this plan: It literally has a huge impact ON DAY ONE.

And it shows that we control our situation… our situation does NOT control us.

I don’t like politicians. They don’t really ever get anything done.

The biggest politician we have today is our Vice President Kamala Harris. She’s accomplished nothing professionally… all she’s ever done is run for office… never even doing the work she was elected to do… always just running for the next office.

Unfortunately this is what Harris knows… and people focus on what they know… so my fear is the swamp just gets deeper with her in office. Ugh.

Another polarizing politician is Alexandria Ocasio-Cortez (“AOC”).

The press loves to paint her as some extremely far left radical socialist. Maybe she is, maybe she isn’t, she represents New York so I don’t know enough about her except the press paints her as some extremely far left radical socialist.

A headline jumped out at me this morning… Kamala Harris and AOC squaring off over a border issue.

My mind raced… it was like two heavyweight politicians in some kind of weird political octagon brawl… which politician could be more worthless?!

AOC opened with a splattering of, well, common sense:

“First, seeking asylum at any US border is a 100% legal method of arrival. Second, the US spent decades contributing to regime change and destabilization in Latin America. We can’t help set someone’s house on fire and then blame them for fleeing.”

But then she just couldn’t help herself and had to go kitchen sink:

“It would be helpful if the US would finally acknowledge its contributions to destabilization and regime change in the region. Doing so can help us change US foreign policy, trade policy, climate policy, & carceral border policy to address causes of mass displacement & migration.”

Throwing in trade and climate policy? And some polysyllabic words? Way to convolute the conversation, AOC!

But, not to disappoint, hammerin’ Harris came back swinging with something even more inane:

“I’m really clear: we have to deal with the root causes, and that is my focus,” the VP said, then added, “Period.”

So the winner is…

…Harris! Spoken like the master politician she is. In other words, if it’s possible, she said even less than AOC… Harris actually said absolutely nothing of substance.

Don Lipsih was all of 24-years young, fresh out of prestigious Colgate University, when he took a small assignment teaching 7th and 8th grade students at All Souls School in little South San Francisco. It must have seemed like a million miles away from his east coast upbringing. As a 12-year old, I, of course, had no concept of just how disruptive this would have been for him… or how courageous he had to be to uproot his entire life and make such a cross-country move.

“Libby” — as we all came to affectionally call him — was without a doubt larger-than-life. At about 6′ 4″ and 300+ lbs., his physicality was amplified to we diminutive 7th graders. A giant, enormous teddy bear.

But it wasn’t his physical stature that made him special… it was who he was: The best teacher I’ve ever had. And more than that, one of the best people I’ve ever known.

One of Libby’s incredible talents was blending seemingly contrasting behaviors. He was quick to laugh, but equally as quick to take whatever grandiose statement a 7th grader was trying to make with utter seriousness. He gave you the respect of an equal, but there was never a doubt of who was in charge. He loved good-natured ribbing, but he also taught us that there were very bright lines in the world that could never be crossed.

The contrasts always made for surprising, refreshing, and interesting exchanges… but ones that never caught you off-guard. Lib, always kind and considerate… always the gentleman… wouldn’t do that to someone.

Most notably, Libby had perspective and wisdom. He was, in fact, the wisest man I’ve ever known. I don’t mention this lightly, most of us spend a lifetime searching for these qualities and never really get there. Lib had them in spades at 24!

As my life-long friend John Marino recently intimated, he changed an entire community of people forever.

Another life-long friend, Dave Rosaia, chimed in that he was the rare educator that actually cared about his kids. High praise coming from a persona that sent lesser teachers ducking for cover.

But Libby didn’t just teach us. He became our friend. I can’t even count the times a half dozen of us would pile into his big ‘ole, bright mustard yellow, larger-than-life Delta 88 convertible and go golfing or to the movies or such.

And he didn’t just have that effect on students, the entire community loved Libby. He was possibly the most beloved person I’ve ever known, too.

And richly deserving. His superpowers were that he made everyone feel special… and, even more appreciated, safe. He simply let you be you. Incredibly uncommon qualities.

Teaching wasn’t paying all the bills, so he eventually augmented his salary with a bit of catering out of his kitchen — I believe his first business name was something haphazard like “Vittles Unlimited.” My little sister Lisa was helping him on the weekends. Libby brought his Libby magic to every relationship and his small business couldn’t help but grow. It grew so much that, at one point, Lisa had a team of three adults working for her… and she couldn’t even drive yet… if another party needed her, she would literally point to an adult and say “drive, please, now!” Libby knew how to recognize… and unlock… potential, another superpower of his.

Libby’s business grew so much that he was able to buy a flailing catering company that had a great store front location and rebranded his business to “Continental Catering.” He definitely stepped out of his small kitchen and into the big time. It was the 80’s and Silicon Valley was experiencing a second great technology wave. With companies like Apple and Intel making a fortune in tech, Libby was making his fortune running each and every shindig they threw.

Around this time I remember Libby shedding about 100 lbs (!)… and when he hit his goal weight, he bought himself a brand new, totally fancy, totally cool, ivory-colored Porsche 9-2-4. We were, of course, all in awe. :)

Even with the weight loss, the rigors of catering eventually took its toll on his health. And so he retired early… leading what I can best describe as a “wealthy vagabond” existence. He once told me, “if I’m driving past an airport and decide I want to have lunch in Paris, I just pull into short-term parking, buy a plane ticket, and just go. Anything I need I just buy along the way.”

I experienced this firsthand in the most dramatic and surprising way. My wife and I got married in Greece, bringing just our immediate families and our best man & woman with us. And, of course, Elle’s soon-to-be-godfather Uncle George. Next thing I know, Libby shows up at the wedding! In Greece! Totally unannounced! It was an entrance to beat all entrances.

It was incredible to hear his stories… but there was a sadness, too. The only family he had was an aging mother. He never married, in fact I never even heard him mention a significant other… friends or otherwise. I worried that he was alone in the world.

To this day, I’ve never been able to reconcile that. I’ve never known somebody so loved by so many… just kinda dropping off the face of the earth. It was if he gave so much of himself for so long… that it was impossible for him to give anymore.

We grew distant over the years. Not his fault, mine. Another life-long friend Frank Fano and I always threatened to descend on him some weekend, but we never did. For me, I think it was because I always dreamed of reuniting with Lib in a triumphant way… to talk about amazing and great conquests in business. But, with a schoolboy mentality, I hadn’t yet felt I had achieved anything that would make him truly proud of me.

But I didn’t think time would run out. Stupid schoolboy me.

Years ago I closed down the Oasis Bar, located a few blocks from his catering storefront, and left him a, “how ya doin’, Lib?!” note… to which his reply included:

“It’s always great to hear from you, even if it’s a card in the door. I’m going to be a very old man before I see you again I think.”

He was, among all his incredibly qualities, simply insightful. He knew.

A few years back — when Lib would have been looking up at 70 — and on the occasion of my 57th birthday — I bucked up. I pulled out another letter he wrote me… one that I had been trying to answer for many years… and was determined to finish my reply to him. It was well past time I told Libby just how much he meant to me.

It was the most personal letter I have ever written… written to the person that believed in me before all others.

Some of it was apologetic, the student worrying about disappointing the teacher. But here’s the part I’d like to share… because I believe it may capture some of what we all felt:

~~~~~~~~~~~~~~~~~~~~~~~~

I never saw the movie, “To Sir With Love.” But the song by Lulu is one of my favorites… in particular the closing verses:

A friend who taught me right from wrong And weak from strong That’s a lot to learn, but, what can I give you in return?

If you wanted the moon I would try to make a star But I, would rather you let me give my heart To Sir, with love

I was always bummed that this was written from a girl student to a male teacher… because it’s not a very manly thing to share with another man… but the importance of the sentiment is dead-on for me.

At this point in my life, I’m not sure what I can give you except the knowledge that you have been in my heart every day since the morning you walked into our 7th grade classroom. More than a mentor… a father.

Nobody likes Trump. He acts like an idiot. He’s divisive and an awful communicator. He doesn’t inspire trust. He’s arrogant, bombastic, and narcissistic. About as un-presidential as you can get. He’s embarrassing.

I, literally, can’t stand the guy.

He, literally, chased me out of the republican party.

However, here’s what I’ve learned from the last four years: No matter how bad Trump was — and he was awful — he still ran circles around all the other politicians.

Why? Because he got things done. As opposed to politicians, who are too busy, well, being political… i.e., doing and saying whatever they need to to get elected. Because that’s their profession… running for office.

And, once elected, politicians don’t do anything… they just work on getting elected to their next post. Or re-elected to their current post. Because they’re not trained to do anything but run for office.

Those are — in general — the folks we have running the biggest country in the world.

It turns my stomach that career politicians — democrat or republican — are the best we can do.

Trump was different, though (queue the giant “understatement” look). He wasn’t a politician. In fact, he was a political idiot. But he got things done. China has been ABUSING us for decades. Clear as day. Yet there wasn’t a single politician — like ever — that did what Trump did: Call them out on their bullshit. Because, if you’ll recall, that was really politically unpopular when he first started pushing. “Oh, a trade war will cause the stock market to crash! Oh, everything will be more expensive! Oh, how can we be so insensitive to a developing nation?” Bullshit.

And he called a spade-a-spade with China and Covid… and about WHO bias… both resulting in an unbelievable outcry… but both positions proving to have merit. As did closing the airports to China travelers… hugely unpopular… until the whole world followed suit weeks later. Ironically, after getting blasted for being “jingoistic,” Trump then got blasted for “not doing enough soon enough.”

I hated that he trashed the Paris Accord… and I still do… but Trump was right to point out that the agreement was unfair, that everyone else had to start their hard work, but China and India — the two TOP emitters in the world — could actually increase emissions under the agreement?

Huh? That only isn’t fair, it’s dangerous.

But that’s what most politicians do — head-scratching things — because they’ve never really run anything… because all they know how to do is run for office.

Trump was the first president in modern memory to propose that government employees not get automatic raises, but rather, get compensated based on performance. That was really unpopular, too. But smart, when is rewarding mediocrity a good thing?

Trump bypassed normal and ineffective bureaucracy and directly tweeted to China and Russia that military spending was “crazy!”… something that a politician would never do… but in one bold stroke, moved the reduction of military spending to the top of the agenda. Because military spending is insane.

And speaking of military spending, what about NATO? Trump was the first president to have the audacity to hold every nation accountable for the commitments they made… to pay their fair share.

Trump was an idiot on the whole wall thing, but he was right that we have a problem with illegal immigration.

In fact, that was so much of Trump’s problem… that he simply acted like an idiot… that his behavior simply got in the way. I absolutely stopped reading – – caring — about anything he said or wrote unless it was a topic of substance… because about 98% of what he said was narcissistic, immature gibberish.

But… he wasn’t a politician… and, for me, it was eye-opening what a non-politician could do in government.

You would think we could find a few candidates with both real management AND diplomacy skills — and the desire for public service — among 330 million Americans. Instead we’re stuck choosing between embarrassing or ineffective. Unfortunately, as difficult as it is to stomach — AND IT IS — embarrassing trumps ineffective.

So, on this inauguration day where two more politicians will get sworn into office, I fear, yet again, that we’re going to be led by people who are non-doers.

And that’s what’s wrong with government… electing officials that know how to kiss babies… but don’t have the skill set to manage big things.

And one other thing: We knew exactly what Trump was when he got elected… warts and all. That’s why seemingly reasonable and rational people backed a political idiot… because they knew what they were getting… as opposed to yet another politician simply telling them what they wanted to hear.

Many years ago, someone termed the new leadership in NASDAQ “FANG”… Facebook, Amazon, Netflix, and Google. Essentially the best of the new tech.

Over the last few years, that morphed into “FAAMG”… Apple and Microsoft got let into the group. While elder statesmen, there is no doubt that they deserve to be part of tech’s elite.

So powerful is this group that just those five stocks represent 20% of NASDAQ movements. That is incredible, if not incredibly unbalanced.

And it’s the performance of these five companies that have kept the NASDAQ index from falling like other popular indexes around the world.

For four out of the five companies, the performance has been merited.

We all have to stay at home and have things delivered to us? Geez, could it get any better for Amazon (AMZN)?

We all have to stay at home and use the cloud to do pretty much everything in our lives… like work… school… socializing… entertainment? That’s great news for cloud-based leaders like Facebook (FB), Microsoft (MSFT), and Google (GOOG).

So why am I separating Apple (AAPL) from the herd? After all, our mobile device is absolutely indispensable, right?

Yes, but will people without jobs… without income… scared and uncertain when the crisis will be over… line up for new iPhones come this fall?

I don’t think so.

That is, if there’s even an Apple Store open to line up in front of.

No other FAAMG’s business is taking a hit like this… to the contrary, all the other FAAMG’s businesses are being helped by the crisis.

It’s not Apple’s fault that the entire world just stopped. But it is investors’ fault if they invest in Apple right now. Because — right now — Apple is getting gutted.

So why is AAPL enjoying the same stock success as these others? To borrow a phrase from a past crisis: Irrational exuberance.

Apparently China has punitively banned 35% of beef imports from Australia… because the Australians haven’t backed down on their questions to China about the origins of Covid-19.

And this just days after China floated plans to do an 80% tariff on Australian barley… which apparently completely derailed the trade.

China must be so proud of its Communist Party.

This is the kind of thing that could — should — blow up in their faces.

This is from a KeyBanc Capital Markets report, using internal credit card data, as reported by ZeroHedge.

Here’s the mind-boggling chart. Notice there is no “black bar” for April 2020 store revenues. Uh, oh.

Another uh, oh: That light gray bar for April 2020 is the same size as March 2020 — meaning no growth in online sales month-to-month — and is noticeably smaller than April 2019 online sales.

So, so much for Apple’s online sales picking up the slack for their closed retail outlets.

There’s data, in no black or white!

So how in the world could Apple continue sprinting towards an already inflated all-time high?

Warren Buffett almost single-handedly put a stop to the last financial crisis in 2008. He penned a now legendary “Buy American. I am.” op-ed in The New York Times. That was incredibly significant. It gave investors the confidence needed to get back on the horse. If getting back in the market is good enough for Warren, it’s good enough for me!

Yesterday he may have done just the opposite.

At the Berkshire Hathaway annual meeting, Buffett informed, well, the world that he completely liquidated his significant airline holdings.

Too much uncertainty.

Translation: I’m selling because I think things will go down.

Commenting on Apple’s financials is like complaining after someone just bowled a 300. They really are perfect.